Adventurous Growth: The stock market strategy for the ambitious

The Adventurous Growth investment style lends itself to high aspirations.

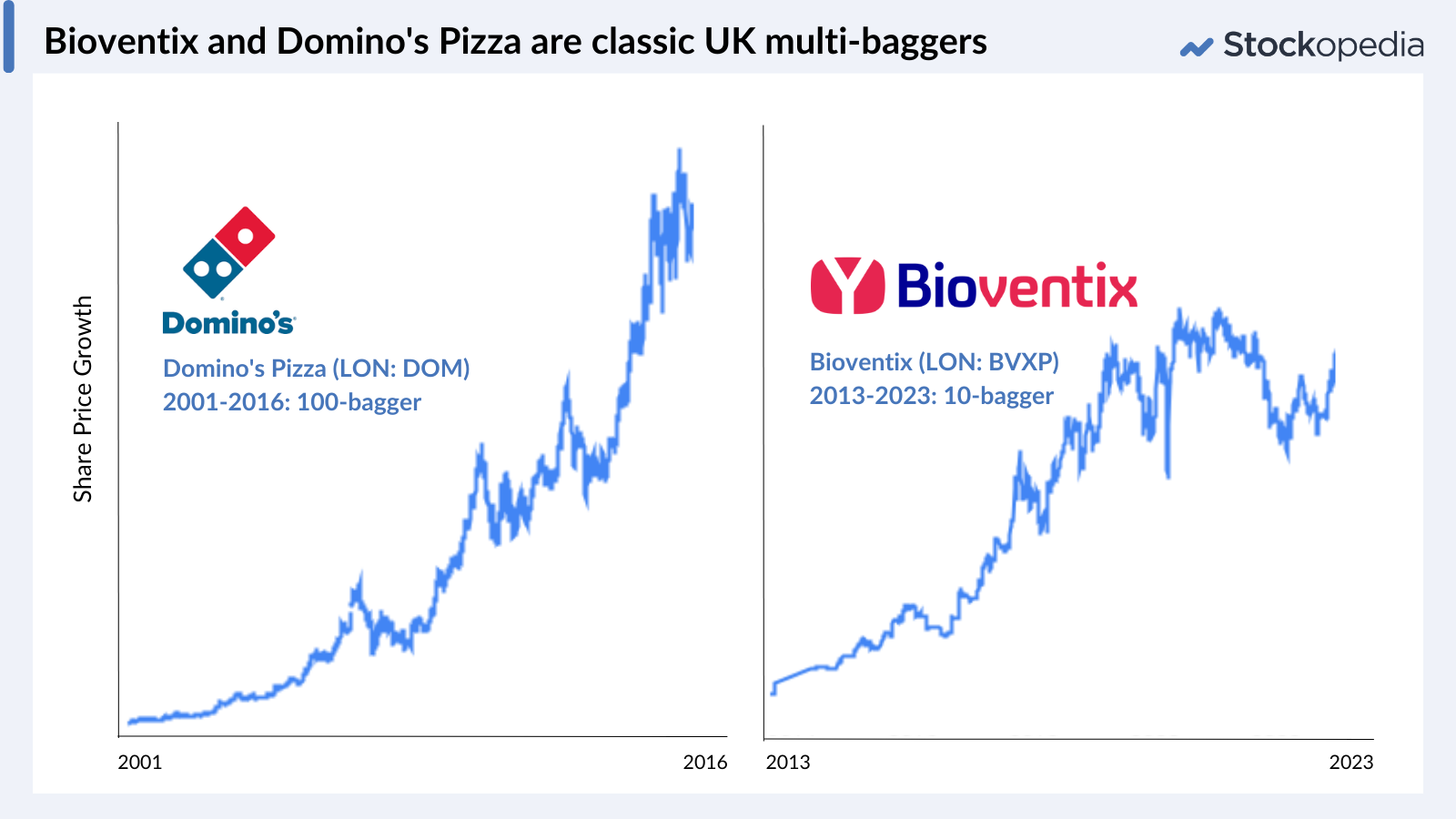

For a start, there are the anecdotes. How many of us have heard tale of the private investor who bought Domino’s Pizza or Bioventix soon after their respective IPOs?

Then there are the stars of the strategy, whose success is something that we would surely all like to replicate. Peter Lynch, for example, who retired at the age of 46 having managed a portfolio which generated annual returns of 29% over 15 years. And Bill O’Neil whose success in growth investing made him enough money to buy himself a seat on the New York Stock Exchange at the age of 30 - the youngest person ever to do so.

And let’s not forget the profile of the stocks which fit into this style of investing: multi-baggers (a Peter Lynch term which defines a stock that returns more than 100%). These companies are leaders in their field, they are doing something new and exciting and they are capturing headlines for both their intrinsic growth (driven by the quality factor) and their share price (momentum factor).

But for every promising stock which flies to multi-bagger status there are many more which flop. Adventurous growth investing is therefore not for the faint-hearted. This guide will:

- Help you understand what it takes to be a successful growth investor

- Explain the fundamental drivers behind growth investing

- Introduce you to some successful growth investing strategies

- Help you formulate a growth investing strategy which works for you

Are you a growth investor?

There is no doubt that all investors, regardless of their mindset, want the same outcome from the stock market: to make money. But the process by which they go about profiting from the stock market can be divided roughly into two camps: those who hunt for value and those who hunt for growth.

But there is nuance in those camps which means that the investor mindset from value to growth is more of a spectrum than a clear defining set of principles. At one end are the deep value investors who seek companies whose shares are currently trading below their intrinsic value, regardless of what that intrinsic value might be. These investors rely on mean reversion - that undervalued shares will eventually revert to the mean and become fairly valued. It’s a highly successful method for stock picking, which we have written about in detail here.

And at the opposite end of the spectrum are the adventurous growth investors. Those who believe that high growth quickly outweighs the advantages of an undervalued stock with no growth potential thanks to the power of compounding. High growth investors believe that corporate innovation will lead to changes in the way industries function in the future - they are, in other words, betting against mean reversion.

Interestingly, these two extremes of investing suit those with similar traits - deep value favours the brave, growth favours the adventurous - and it can be tempting to assign yourself to one of these camps based on the traits you perceive as favourable. But in both cases it’s important to recognise the limits of mindset: bravery in the quest for value stocks can become foolishness; adventurousness in the quest for growth stocks can become recklessness.

Instead, to be a successful growth (or deep value) investor, it is useful to understand what drives the strategy. We have written in detail about the Deep Value drivers in this article and you can read on here to find out more about growth investing and how to assess whether it fits your profile.

Why growth investing works

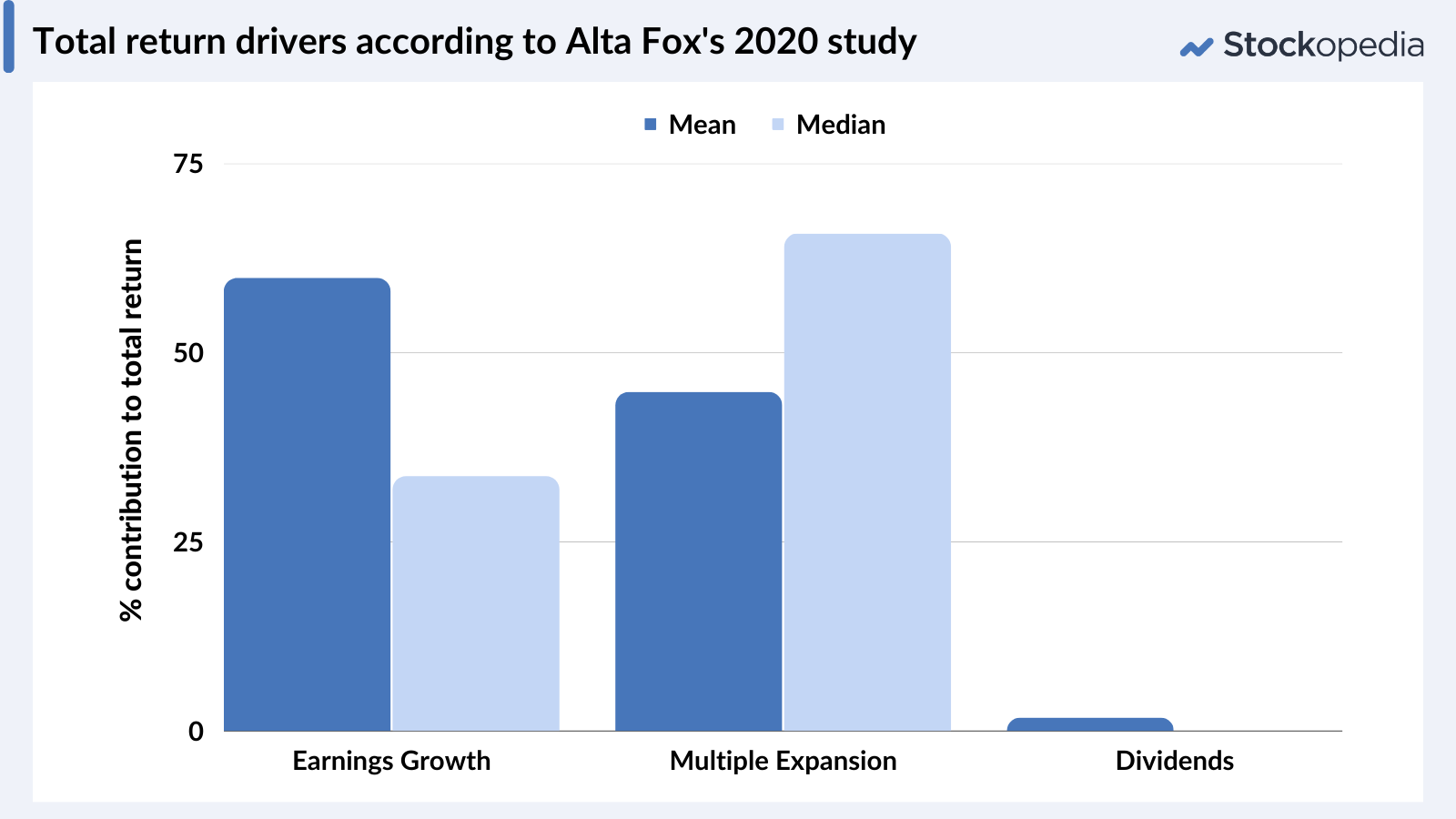

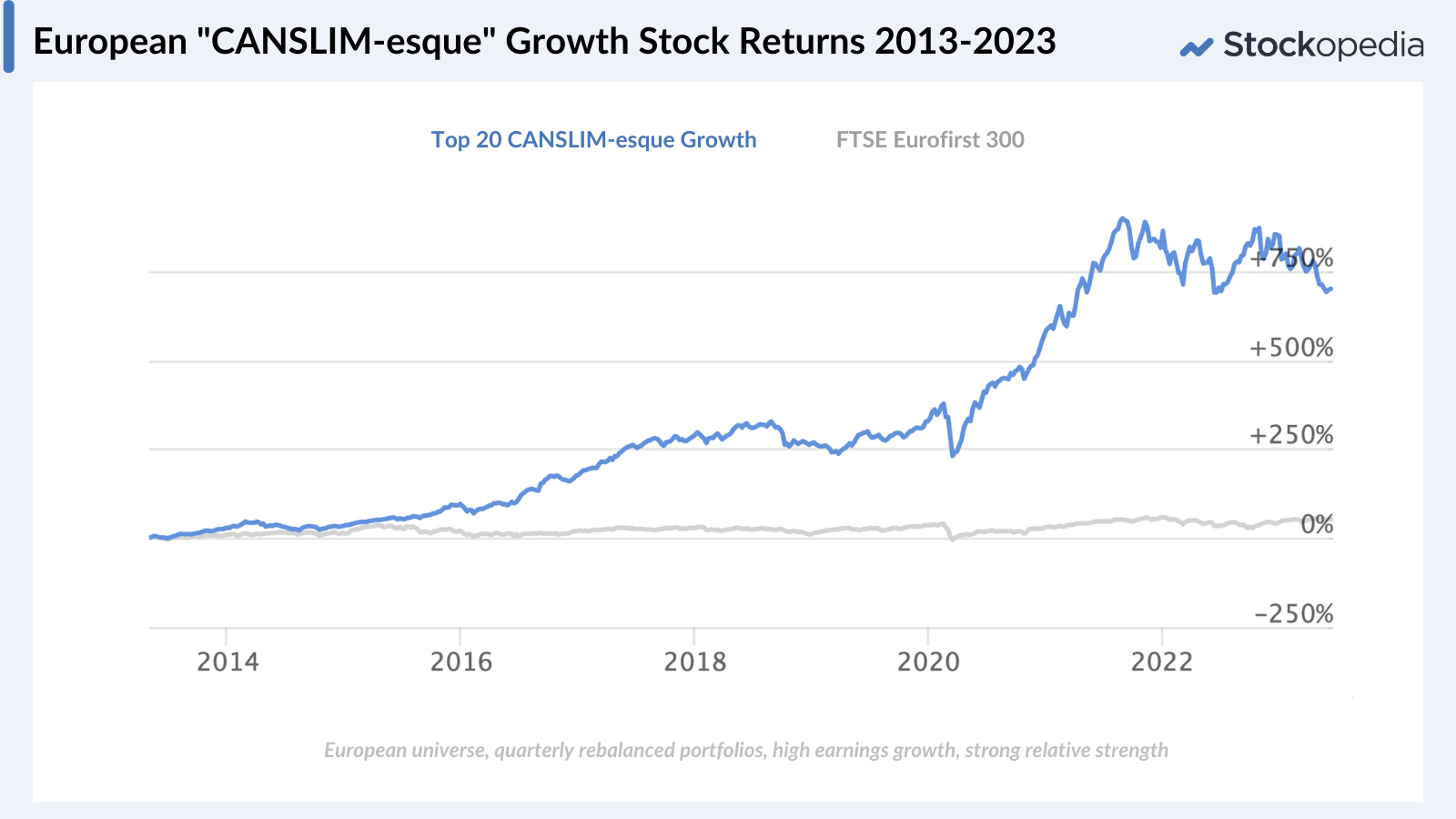

Stock price increases happen for two key reasons, earnings growth and multiple expansion, and the contribution of both of these elements was assessed in a 2020 study by US asset management group Alta Fox.

In the study, researchers screened for companies in the US, Western Europe and Australia with a market cap between $150m and $10bn which had a total shareholder return of more than 350% in the five years to August 2020. The researchers conducted a deep review of the 104 companies (14 of which were listed on AIM) which emerged from the screen and found that earnings growth and multiple expansion played a roughly equal role in driving total returns over the period (dividends provided nothing).

Drilling down into each of those two drivers in turn provides a useful overview of the type of qualities that growth investors should be looking for from their stocks.

Earnings Growth

Earnings Growth relates to the fundamental growth being driven by the company’s operations. It goes without saying that growth companies should exhibit top line strength - the Alta Fox study found median revenue growth in its 104 top growth companies of 113% over five years. But what is perhaps surprising is the extent to which acquisitions helped drive that growth. Over half of the companies in the study made a transformative acquisition in the period under review, while only 27% launched transformative new products. The proportion of companies (80%) which issued new shares in the period is perhaps linked to the level of acquisition. Almost a quarter of the companies in the study diluted their shares by more than 50% and 11 diluted by more than 100%.

But acquisition alone (or indeed transformative product launches or new contracts) is not enough to drive reliable growth over the long term and this is a key point which distinguishes high quality growth investors from short term momentum chasers. Investors hunting for sustainable growth should focus on businesses with efficient capital deployment and strong returns from their investment.

For revenue growth to be enduring and sustainable, companies also need to have strong operating leverage - an ability to easily increase profits by increasing revenue. Companies with high operating leverage have low variable costs, which means higher demand doesn’t require greater operating expenditure. That observation might provide some explanation behind type of companies which fit the high-growth profile. Alta Fox found that over half of its high-growth companies were in the technology and healthcare industries - both industries with high margins and operating leverage.

Overall, Alta Fox’s 104 companies reported average annual earnings (EBITDA) growth of 28% over the five years leading up to the study’s publication.

Key Metrics: Earnings Momentum

- Revenue Growth: Growth companies are going to struggle to provide sizeable returns without strong sales momentum. Investors should look for double-digit compound annual sales growth at the very least and sales growth in the most recent interim announcement as well.

- Operating Margins: It is hard to provide a definitive level for operating margins because some industries lend themselves to much wider margins than others. When it comes to growth companies however, high operating leverage (which can be identified through high operating margins) is key and so a general rule of thumb is to look for companies with an average operating margin greater than 20%. However what is most important is consistency in those operating margins - avoid companies whose operating margin is narrowing.

- Earnings Growth: Earnings per share are calculated by dividing a company’s net profit by the number of shares in issue. Many companies like to give adjusted or diluted figures, but it is important to assess the actual numbers when hunting for growth. Investors should look for businesses which have a track record of double digit annual earnings growth, plus year-on-year growth in the most recent interim earnings. Return on Equity (ROE): Calculated by dividend a company’s net profits with the average book value for the period, ROE is a measure of how efficiently a company is using shareholder capital. Investors should look for a long-term ROE of more than 10% and (just as with operating margins) should avoid companies which have suffered a recent drop in ROE.

Multiple Expansion

It should be said that while an adventurous growth strategy leans heavily on the quality and momentum market drivers (good stocks beat bad stocks, strong stocks beat weak stocks), it is important not to overlook the role valuation plays. And that is because of multiple expansion.

Put simply, multiple expansion refers to a rising valuation multiple, for example the price to earnings ratio, over time. Multiple expansion happens because investors are willing to pay higher multiples for fast growing companies.

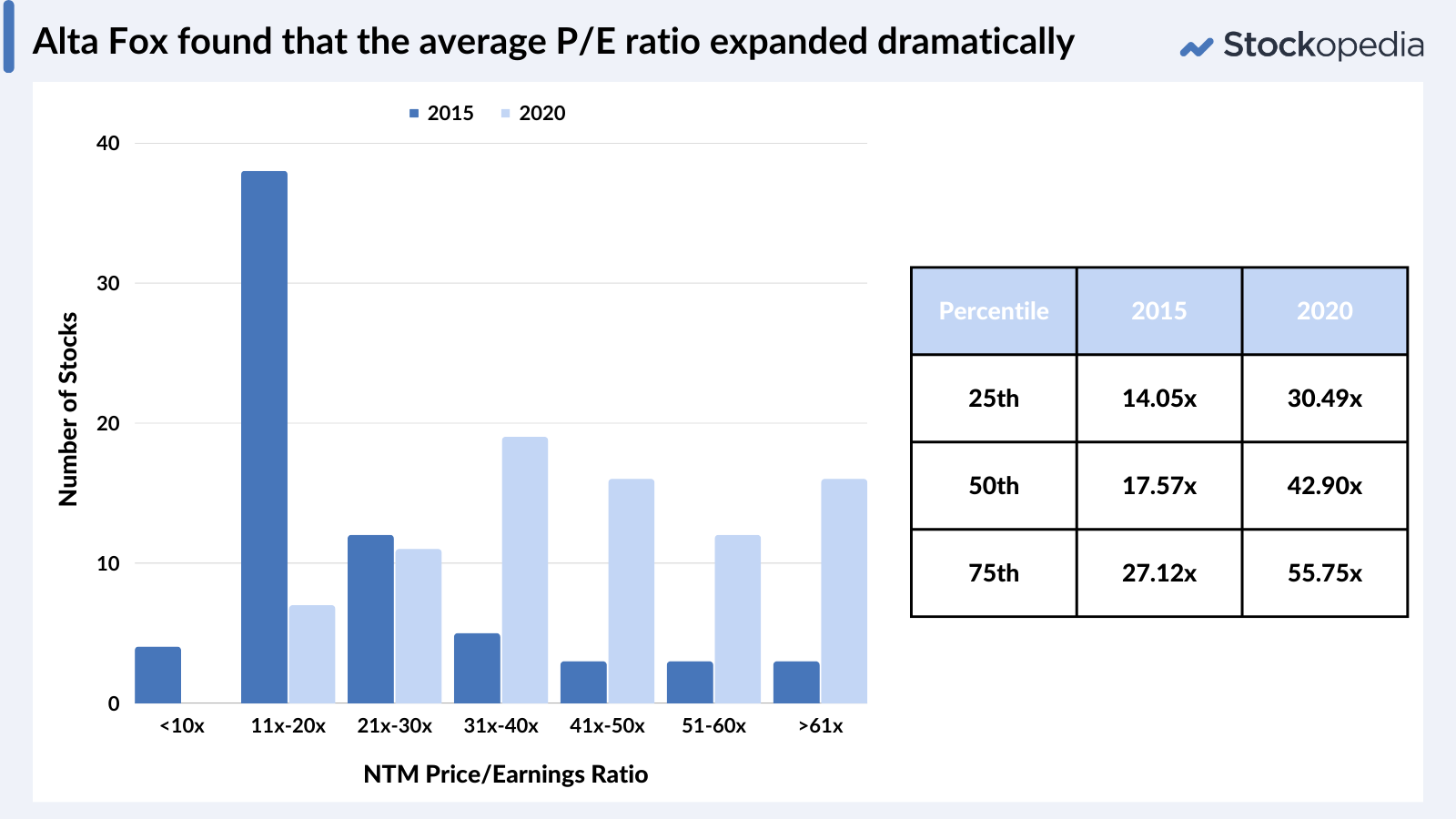

We can see in the chart below that in 2015, the average price to earnings (PE) ratio of the 104 stocks in the Alta Fox study was 17.6 - not alarmingly expensive. But by 2020 when the study concluded the average PE ratio was 42.9. Over the five years included in the study, only 11 of the 104 companies failed to report multiple expansion.

It’s this phenomenon which explains why growth gurus like Jim Slater include valuation metrics in their stock selection process. For a stock to grow it needs to come from a starting point where its valuation is not being reflected in its growth potential. In other words it is important to buy something at a meaningful valuation if you want to see these multiples expand.

Key Metrics: Multiple Expansion

- Price to Forecast Earnings Ratio: The PE Ratio is calculated by dividing the current share price with next year’s expected earnings per share. For growth investors it’s important not to get hung up on this metric (many growth companies trade on seemingly high valuations), but it is also important not to overlook it. There can be no one definition of an appropriate PE ratio for growth stocks, but investors should compare it to the quality metrics of the business and the growth on offer.

- PEG Ratio: Jim Slater pioneered the use of the price to earnings to growth (PEG) ratio in the UK through the publication of his book ‘The Zulu Principle’. It is calculated by taking the historic PE ratio and dividing it by forecast growth. Slater looks for companies with a PEG of less than 0.75. In modern markets it is hard to identify many quality companies with such a low PEG ratio so common sense is needed. Relative strength: Multiple expansion relies on share price growth which can be assessed by looking at the price strength compared to the market. Investors should look for three, six and 12 month relative strength of more than 0%.

Will growth investing work for you?

All this being said, it’s time to return to the traits necessary to be a successful growth investor:

- Diligence to hunt for promising growth stocks using fundamental (and sometimes technical) analysis).

- Patience to let earnings compound and multiples to expand over time. Growth investing is a medium to long term investment strategy, not suitable for those looking to make a quick return.

- Discipline to form a strategy and stick to it.

- Ambition to identify game-changing stocks. Growth investing is about identifying stocks with immense potential, beyond the numbers that are being reported now.

How to implement a successful growth strategy

Look back over the history of growth investing and you’ll find names like Thomas Rowe Price and Phil Fisher. Warren Buffett even pops up now and then because - though he was a strong proponent of the teachings of deep value investor Ben Graham - he professed that value and growth investing are “joined at the hip”.

In the late 1990s the likes of Bill O’Neil and Peter Lynch (in the US) and Jim Slater (in the UK) added their names to the list of successful growth investors. And more recently fund managers like James Anderson (from the Scottish Mortgage Investment Trust) and traders like Mark Minervini have joined the roster.

But aside from the fact that they seek growth and have been very successful, these pioneers of the strategy don’t have an awful lot in common. The truth is there can be no one definition of a growth strategy. For some investors, growth means buying companies when they’re small and holding onto them until they’re big, for others it means riding the wave of high quality shares that are on an upward streak and yet others look for stocks whose earnings potential is not currently being reflected by the market capitalisation.

The important thing is that you need to find a style of growth investing that suits you and learning from the gurus of the past can help you do that.

Peter Lynch: Buy what you know

Reading the millennium re-print of Peter Lynch’s famous book One Up on Wall Street (first published in 1989) today is fascinating. By 2000, Lynch had been retired from fund management for a decade and he talks in his introduction about his experience as a private investor during “the greatest bull run” which started in 1982 (and, at the time the introduction was written, hadn’t yet collapsed into the Dotcom bust).

For someone so adept at beating markets with a high growth strategy it would be easy to assume that at the turn of the millennium Lynch was riding the wave of internet mania, but he admits in this re-print to being a technophobe. “So far the internet has passed me be,” he writes. He talks of Amazon.com becoming a ten-bagger in one year (1998) and comments (disdainfully) on the fact that internet companies could reach market capitalisations of over $1bn before having even turned a profit: “the mere appearance of a dot and a com is enough to convince today’s optimists to pay for a decade’s worth of growth and prosperity in advance,” he says.

For Lynch, growth investing never was about jumping on the bandwagon (or as he calls it “being trendy”), it was about identifying quality stocks with excellent fundamentals which, crucially, were easy to understand. In 2000 “despite the instant gratification that surrounds me”, Lynch was still investing with these fundamental principles at the heart of his strategy:

- Don’t invest in stocks you don’t understand and don’t hold any more stocks than you can remain informed on (Lynch himself said as a private investor he kept tabs on about 50 stocks).

- You don’t need to make money on every stock you pick, especially not immediately. It generally takes three to 10 years for investments to play out.

- Understand where a company is in its expansion phase - a retailer which already occupies 90% of its market has a very different profile to one which only has 10%.

- Look at debt to assess whether a few bad years would hinder long term progress.

- Don’t get scared out of stocks and don’t over-read the news.

Jim Slater: The power of the PEG

Just like his peers in the US, Jim Slater sets out his growth investing strategy with a strong warning to improve your understanding of the stock market before buying. But unlike the strategies mentioned above, Slater’s Zulu Principle can be followed on screening alone. We have created our own version of the Zulu Principle screen which you can use here.

His strategy leans heavily on the two drivers of growth: earnings momentum and multiple expansion. His criteria (which we have turned into a screen which you can see here) are:

- High quality earnings growth: Growth companies need to be growing their profits at a decent pace and be able to generate a strong return on their own re-investment in the business. Slater identified this using the return on capital employed (ROCE) metric and hunting for stocks with a trailing 12-month ROCE of more than 12%. He also looked for stocks with rolling earnings growth of at least 15%.

- A valuation with room to expand: Aligned with the principles described in the Alta Fox study (above), Slater looked for companies with a sensible price to earnings (PE) ratio which isn’t taking into account for the company’s forecast growth. He set an upper limit of 20 times forecast earnings and also pushed the use idea of the PEG ratio as a great way of identifying growth stocks - growth, that is, at a reasonable price. The PEG (price to earnings to growth) ratio favoured by Slater is less than 0.75.

In addition to these traditional drivers of growth, Slater also encouraged private investors to find their own niche - something that would give them an advantage over asset managers with a great deal more capital and resources. The conclusion: focus on smaller companies.

Bill O’Neil: CANSLIM

Bill O’Neil is famed for being one of the first investors to use data analytics at the heart of his investment process. He built a strategy known as CANSLIM - an acronym of the seven traits which he deemed most important for a stock to grow in value. These are:

- Current Quarterly Earnings per Share (EPS) up strongly (more than 20%) on the same quarter in the prior year.

- Annual EPS increases of more than 20% over the last three to five years.

- New products, management or an event which could act as a catalyst for further growth.

- Scarce supply, but a strong appetite for the shares.

- Leading companies which are the pioneers in their market.

- Institutional interest in the shares.

- Market direction pointing upwards.

Now some of these ideas are numeric meaning they are quite easy to screen for (we have created a Bill O’Neil screen which you can use here). All investors can set up their own screen to whittle down stocks which are growing earnings both in the short term (quarterly) and over the last three to five years by more than 20%. It’s also possible to identify stocks where shares are in strong demand - demonstrated by positive absolute share price strength. Institutional interest and strong market growth are also easy enough to identify (although not so easy to screen for). It’s in the hunt for leading companies which have something new to report that investors need to apply a bit of discretionary, qualitative analysis.

Richard Koch: Star Principle

In complete contrast to Slater’s Zulu Principle, Richard Koch’s Star Principle focuses on two completely qualitative qualities of growth companies. Koch is an entrepreneur and venture capital investor and his book can certainly be viewed through that lens - he talks about building fast growth businesses as well as investing in them. But the lessons still apply. For stocks to be classed as ‘Star Businesses’ they need to meet just two criteria:

- Be a market leader

- Operate in a high growth market

The logic for these criteria is simple. Market leaders should be able to charge higher prices than their peers because they sell products or services that are favoured by customers. It’s important therefore to be a leader in a niche market, where replicating the success of the products or services is not something that can be done easily. And the reason that the market needs to be growing is to allow the company to expand in size - it’s no good growing if the prospects are going to be stifled by the potential size of the market.

How to implement a growth strategy: a step-by-step guide

Step 1: Are you a growth investor?

First up, you need to understand whether growth investing is the right strategy for you to pursue and how much of your portfolio you want to assign to growth shares. To do this, remember that profits from a growth strategy can take time to materialise so don’t invest any money that you are going to need within five years.

You also need to define what type of growth investor you are. Are you looking to take bigger risks (in the hope of greater rewards) by employing a fully qualitative strategy like Richard Koch, or do you want your returns to be driven by reliable earnings growth in a style that reflects Peter Lynch? A blend of both approaches is fine, but it’s important to ensure that higher risk stocks only ever form a small part of your portfolio.

Step 2: Set up a screen to identify growth companies

At Stockopedia we already have some ready-made screens based on the Bill O’Neil and Jim Slater investment methods. Or you can set up your own screen which blends the growth metrics (listed above) that are most important to you.

You can set tough restrictions on your screen to identify stocks which exactly match your criteria but beware that some short-term blips could exclude interesting stocks from your screen. Alternatively loosen the screening metrics to leave yourself with a long list of possible stocks for further analysis.

If you are a fully systematic investor, your screen should provide you with a list of stocks that you would be happy to add to your portfolio with very little further research. But even if you are following a fully systematic strategy and being led by the screen, you should check stocks for any major flaw that you are uncomfortable with (but try to ignore psychological biases).

Step 3: Discretionary and market analysis

Most growth investors would do well to add some discretionary and markets analysis to their process as no screen will ever be able to determine whether a stock is a market leader. Check the financial reports of the company and its peers and compare recent performance. Understand how the company has grown in the past (acquisition or internal development) and assess whether that growth potential still exists. It is also useful to spend some time looking at the market in which the stock operates - is the market itself growing and is there any new competition which should be feared?

Step 4: Set a routine for buying growth shares

When you’re building your portfolio look to add shares every few months, building a regular cadence for buying until you reach a sensible sized portfolio. Unlike other strategies, a growth portfolio doesn’t necessarily need full sector diversification (some sectors don’t lend themselves to growth investing at all, while others offer many opportunities for growth stocks). You should aim to build a portfolio of at least ten companies, diversified across a few different industries.

Step 5: Keep monitoring your shares

Keep monitoring the stocks in your portfolio for any change in performance. Some growth stocks become quality compounders which can be held forever (you can read more about that strategy here), but for others, the investment case can come crashing down when the growth stops. In many cases that is because of a maturing market which has no further room for expansion. Set yourself a routine for checking your portfolio stocks (not too regularly) and use quantitative (unemotional) metrics to assess whether anything has gone awry.

Step 6: Enjoy it!

Building and managing a growth portfolio can be enormous fun. Make sure you enjoy it.

Risks and Limitations of the Adventurous Growth Strategy

Every stock market strategy comes with its own share of risks and Adventurous Growth is no exception. Here are some of the major concerns:

-

The growth stops

Not all companies can continue to grow indefinitely. Some continue to be market leaders, generating reliable revenues, profits and cash every year (and can form part of a buy-and-hold forever portfolio). But others face new competition or market fluctuations outside of their control and the share price can come crashing down.

British online retailer Asos is a classic example of an ex-growth stock. Between 2005 (when its factory was destroyed by the Buncefield oil depot explosion) and 2014, the stock 100-bagged. But since then, investors have been taken on a bumpy ride of recovery and disappointment. Without a strong protective moat, the company has been unable to fend off competition from new online retailers and its earnings have suffered miserably.

-

Higher valuations

Investing in high-growth companies often comes with higher valuations, which can increase the risk of significant price declines. Using Slater’s GARP (growth at a reasonable price) lessens this risk, but often avoids the asymmetric payoff type growth stocks seen in big US bull markets.

-

Market cycles

Smaller stocks which can be bought using the GARP principles tend to be more volatile and thus worse affected by the whims and fluctuations of the market.

Closing thoughts

Adventurous growth is the market strategy which gets gets most new investors hooked on stocks. It can be the strategy which propels a portfolio to a decent size, or the strategy which frustrates investors into funds,

Pursuing a growth strategy is not easy and it’s not a strategy which should be taken lightly. But with the right mindset and commitment, adventurous growth can be hugely successful.

Safe investing!

Further Reading

- The Zulu Principle: Making extraordinary profits from ordinary shares - Jim Slater

- One up on Wall Street: How to use what you already know to make money in the market - Peter Lynch

- How to Make Money in Stocks - Bill O’Neil

- Common Stocks and Uncommon Profits - Philip Fisher

- The Star Principle: How it can make you rich - Richard Koch

About Megan Boxall

Disclaimer - This is not financial advice. Our content is intended to be used and must be used for information and education purposes only. Please read our disclaimer and terms and conditions to understand our obligations.

Thanks for that comment @InvestElf - greatly appreciated! We'll be pulling this series into a permanent space quite soon so that they are much easier to find and refer to in future.

Thanks Megan, another great educational resource. I was introduced to The Zulu Principle by my mate Dave in the 1990s and I often look at the screen to see what it finds. One thing that puzzles me though, is that when there are periods without any candidates, the performance chart doesn't have any horizontal lines. I always assumed if no candidate was found at times of rebalancing, then it would go to cash. But I now wonder if it continues to hold previous stocks until replacements are found?

If there are no candidates at the rebalancing date, the chart will flatline. The problem with the Zulu screen is when the market declines there are very few candidates due to the relative strength constraint. I think in the current cohort there are only a few stocks being tracked in the portfolio for the quarter - but it's not empty.

You may find when you view the screen that there are no stocks currently qualifying today, but that doesn't mean there weren't some on the day of rebalancing at the start of the quarter!

Megan,

A truly excellent summary of Growth investing. I was an Growth enthusiastic convert having attended one of Jim Slaters Zulu seminars some 25years ago. And yes I fit the adventurous investing style preferring to buy companies whose earnings and valuation multiple are expanding.

So I was therefore intrigued the read 2020 paper you cite of previous growth companies that had “Multi-bagged” over the previous 5 years. 16 of the 104 companies were from the UK. So back in October 2020 I set up a dummy Stocko Multibaggers portfolio investing a nominal £1K in each of the 16 UK companies, to follow their subsequent progress over the next 5 years. The results to date can be seen below....

My dummy 2020 UK Multibagger portfolio is down -35% from inception and -45% from its mid-2021 zenith. Only one of the 16 companies (YouGov (LON:YOU) is still in profit (+20%) and the worst (Boohoo (LON:BOO)) is down -89%. I have owned (and lost money) on several of the 16 past Multibaggers, but missed out on owning £YOU.

The Multibagger performance drag has been reflected in my own portfolio results, but a couple of years ago I changed tact somewhat. Now about half my stocks are growth companies and the other half are high VM (Ranked 80+ VM) types. This portfolio change introduces some cheaper Value stocks whose “reversion to the mean” is hopefully upward!

thanks Megan - a good read. Probably worth pointing out that in the case of Bill O'Neill's (RIP) CANSLIM strategy that there is a heavy weighting toward technical analysis and buying stocks at the right point coming out of bases or add-on points and also selling/trimming based on price action / breaches of key support areas etc and also focuses on Market and Sector (indeed cites that more than 50% of a stocks price move is related to the market and sector). The market and sector parts are generally quite difficult in a UK setting due to the imbalance of sectors (some sectors have many stocks and others have only a few) and unlike US markets, there is less tendency to trend.

Not sure if the team have done any analysis on breadth indicators and trending them in the UK market (e.g. Net New Highs - Net New Lows, A-D line) - I know you track advances and decliners on a daily basis as its on the home page, but if I want to view the trend of these I tend to go to another site (marketinout).

I have read 4 of the 5 mentioned books (not read Richard Koch's) and would recommend all of them.

*Past performance is no indicator of future performance. Performance returns are based on hypothetical scenarios and do not represent an actual investment.

This site cannot substitute for professional investment advice or independent factual verification. To use Stockopedia, you must accept our Terms of Use, Privacy and Disclaimer & FSG. All services are provided by Stockopedia Ltd, United Kingdom (company number 06367267). For Australian users: Stockopedia Ltd, ABN 39 757 874 670 is a Corporate Authorised Representative of Daylight Financial Group Pty Ltd ABN 77 633 984 773, AFSL 521404.

Excellent, just excellent. This series on investment strategies has finally helped me clear the fog from my fuddled mind after more years as an investor than I care to admit to! You guys have such a tight handle on things, I'm in awe of your collective comprehensive insightfulness and acumen. Thanks Megan and the rest of the team -- awesome!